Search

Relevance of hit: 40%

back to search result indexVolkswagen Group deliveries

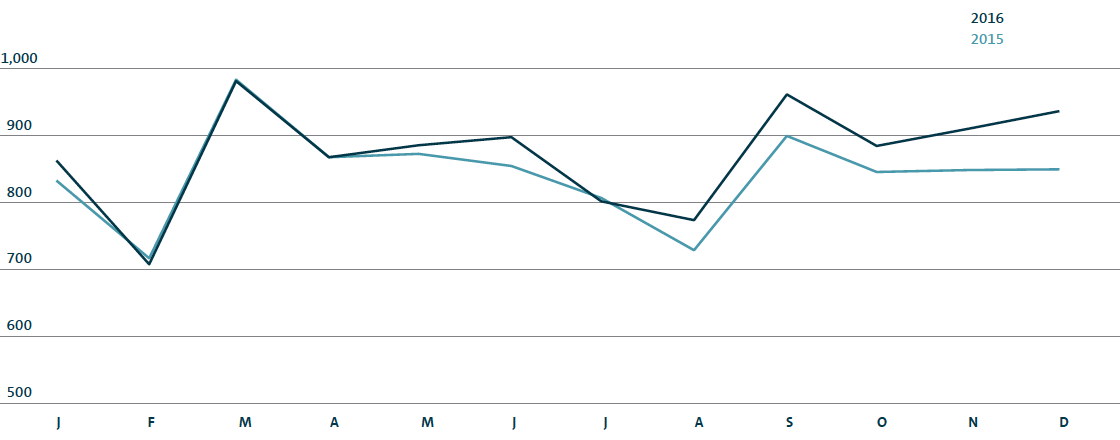

In fiscal year 2016, the Volkswagen Group increased its deliveries to customers worldwide by 3.7% and reached a new all-time high of 10,296,997 vehicles. This means that we exceeded the mark of 10 million units sold for the second time since 2014. The chart on the next page shows how deliveries changed from month to month and compares each monthly figure to the same month of the previous year. Deliveries of passenger cars and commercial vehicles are reported separately in the following.

| (XLS:) |

VOLKSWAGEN GROUP DELIVERIES1 |

||||||||

|---|---|---|---|---|---|---|---|---|

|

2016 |

2015 |

% |

|||||

|

||||||||

|

|

|

|

|||||

Passenger Cars |

9,635,484 |

9,320,687 |

+3.4 |

|||||

Commercial Vehicles |

661,513 |

609,909 |

+8.5 |

|||||

Total |

10,296,997 |

9,930,596 |

+3.7 |

|||||

VOLKSWAGEN GROUP DELIVERIES BY MONTH

Vehicles in thousands

PASSENGER CAR DELIVERIES WORLDWIDE

With its passenger car brands, the Volkswagen Group has a presence in all relevant automotive markets around the world. The Group’s key sales markets currently include Western Europe, China, the USA, Mexico and Brazil. Our wide range of attractive and efficient vehicles gives us a strong position in a persistently challenging competitive environment. The Group recorded encouraging growth in many key markets.

Deliveries of passenger cars to customers rose during the reporting year to 9,635,484 units amid continued difficult conditions in relevant markets such as Brazil and Russia. This was an increase of 314,797 vehicles or 3.4% on 2015. The passenger car market as a whole expanded by 5.4% in fiscal year 2016, which meant that the Volkswagen Group’s share of the global market declined slightly to 11.9 (12.2)%. The Group recorded the highest absolute growth in China. Our sales figures in Brazil, Russia and other countries were impacted by low demand. The diesel issue affected the individual markets, mainly in the USA and Canada, in different ways during the reporting year, depending on the brand. Nearly all brands surpassed the previous year’s delivery figures, with the Volkswagen Passenger Cars brand recording the strongest growth in absolute terms. Audi, ŠKODA, and Porsche set new records, as did Bentley and Lamborghini.

The table on below gives an overview of passenger car deliveries to customers of the Volkswagen Group in the regions and the key individual markets. The demand trends for Group models in these markets and regions are described in the following sections.

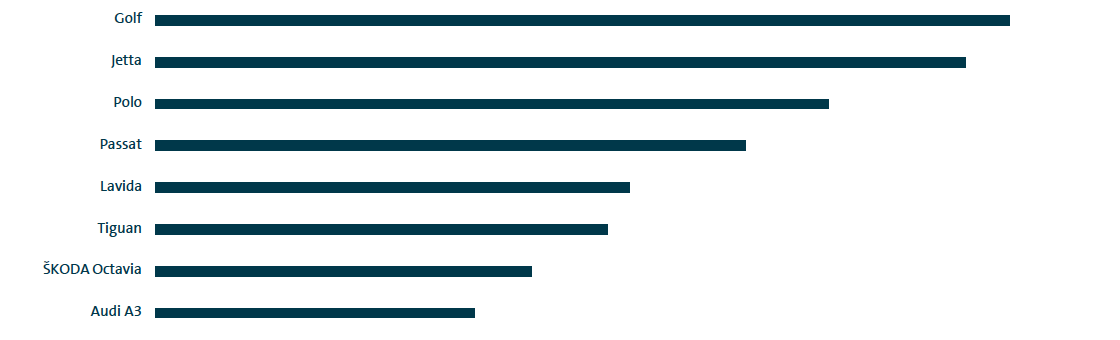

WORLDWIDE DELIVERIES OF THE GROUP’S MOST SUCCESSFUL MODEL RANGES IN 2016

Vehicles in thousands

Deliveries in Europe/Other markets

In 2016, the passenger car market as a whole expanded by 5.8% in Western Europe. The Volkswagen Group handed over 3,114,030 vehicles to customers here, 1.7% more than in the previous year. Demand for Group models was up year-on-year in virtually all major markets in this region. The Touran, Audi A4, Audi Q3, Audi Q7, ŠKODA Superb as well as Porsche’s Boxster and Cayman models saw the highest growth rates. The ŠKODA Fabia and Porsche Macan models were also very popular. The new Tiguan and the new SEAT Ateca were very well received by the market. The Group’s first luxury SUV, the Bentley Bentayga, celebrated its successful market debut. The Group’s share of the passenger car market in Western Europe was 22.3 (23.2)%.

In the passenger car markets of Central and Eastern Europe, which declined overall, we handed over 5.8% more vehicles to customers in 2016 than in the previous year. We recorded growth in almost all markets, with the highest increases recorded in Poland and the Czech Republic. In Russia, the continuing weak economic situation and political tensions caused a decline in our deliveries to customers. Demand was highest for the Polo, ŠKODA Rapid and ŠKODA Octavia models. Our share of the passenger car market in Central and Eastern Europe rose to 21.9 (20.2)%.

In South Africa, the number of Volkswagen Group vehicles delivered to customers fell by 13.0% year-on-year in 2016. The passenger car market as a whole declined by 12.4% in the same period. Demand was highest for the Polo.

Demand for Volkswagen Group passenger cars in the markets of the Middle East region in 2016 was up by 0.7% compared with the previous year. The Polo, Golf, Passat and ŠKODA Octavia models were particularly popular.

Deliveries in Germany

The German passenger car market continued its growth in the 2016 fiscal year, expanding by 4.5%. The Volkswagen Group handed over 1,136,971 vehicles to customers in its home market. This was slightly fewer than in the previous year (−0.9%). The Touran, Audi Q7, Audi Q5 and ŠKODA Superb models saw the highest growth rates. The Tiguan, Audi A4 and SEAT Ateca models were also very popular. In the registration statistics of the Kraftfahrt-Bundesamt (KBA – German Federal Motor Transport Authority), eight Group models led their respective segments at the end of 2016: the up!, Polo, Golf, Tiguan, Touran, Passat, Audi A6 and Porsche 911. The Golf continued to top the list of the most popular passenger cars in Germany in terms of registrations.

Deliveries in North America

In North America, the Volkswagen Group delivered 928,033 vehicles to customers in a slightly growing overall market for passenger cars and light commercial vehicles in the reporting year. This was 0.6% more than in the previous year. The Group’s market share was 4.4 (4.5)%. The Jetta remained the Group’s best-selling model in North America.

Demand for Volkswagen Group models on the US market was down 2.6% year-on-year in 2016, primarily as a result of the diesel issue. The overall market remained steady year-on-year (+0.5%) over this period. Models in the SUV and pickup segments remained in particularly high demand. The Tiguan, Audi A4, Audi Q3, Audi Q7 and Porsche Macan models, among others, registered increases in demand.

In the growing Canadian market, we handed over 5.6% fewer vehicles to customers in the reporting year than in 2015, mainly as a consequence of the diesel issue. The most sought-after Group model was the Jetta, followed by the Golf. The Audi A4, Audi Q7 and Porsche Macan models enjoyed rising demand.

In Mexico, the strong momentum of the market as whole continued in 2016. Group sales were up 12.8% year-on-year. The Vento, Jetta, Gol and SEAT Ibiza models were especially popular.

Deliveries in South America

Conditions in the South American markets for passenger cars and light commercial vehicles were very challenging in 2016. Amid sharp overall declines in markets in this region, the Volkswagen Group delivered 362,343 vehicles to customers, 26.0% fewer than in the already weak previous year. The Volkswagen Group’s share of the passenger car market in this region declined to 10.5 (12.5)%.

In the rapidly deteriorating Brazilian market, 2016 saw demand for Group models decline by 34.6% year-on-year. The up!, Fox, Gol and Saveiro witnessed the strongest sales figures.

In Argentina, the market as a whole continued its recovery in the reporting year. The Volkswagen Group sold 5.6% fewer vehicles here than a year earlier. The Group models with the highest numbers of registrations in Argentina remained the Gol and Suran.

Deliveries in the Asia-Pacific region

The passenger car markets in the Asia-Pacific region experienced the largest growth in absolute terms of any world region in 2016. Demand for Volkswagen Group models there increased by 9.8% year-on-year to 4,282,656 units; the market share in this region was 12.1 (12.4)%.

China, the world’s largest single market, was again the growth driver of the Asia-Pacific region in the reporting year, recording the highest absolute increase. Attractively priced entry-level models in the SUV segment remained highly sought after. The Volkswagen Group delivered 12.2% more vehicles to customers in China than in the prior-year period. The Jetta, Lavida und Sagitar models were particularly popular. The Lamando, Santana, Audi A3, Audi Q3, ŠKODA Superb and Porsche Macan models also recorded encouraging growth rates. The new versions of the Bora, Touran, Magotan, Audi A4 L and Audi A6 L models and the locally produced Golf Sportsvan were successfully launched in the market.

In the growing passenger car market in India, 4.7% fewer Volkswagen Group vehicles were sold in the reporting year than in 2015. The most popular Group model in India was the Polo. The Ameo was successfully launched in the market.

In Japan, sales of Volkswagen Group vehicles were down 8.8% on the prior-year figure. The total market volume declined by 1.6% in the same period. Demand was highest for the Polo and Golf models.

| (XLS:) |

PASSENGER CAR DELIVERIES TO CUSTOMERS BY MARKET1 |

||||||||

|---|---|---|---|---|---|---|---|---|

|

DELIVERIES (UNITS) |

CHANGE |

||||||

|

||||||||

|

2016 |

2015 |

(%) |

|||||

|

|

|

|

|||||

Europe/Other markets |

4,062,452 |

4,006,105 |

+1.4 |

|||||

Western Europe |

3,114,030 |

3,062,371 |

+1.7 |

|||||

of which: Germany |

1,136,971 |

1,147,484 |

−0.9 |

|||||

United Kingdom |

523,111 |

521,345 |

+0.3 |

|||||

France |

249,145 |

252,530 |

−1.3 |

|||||

Spain |

244,990 |

235,141 |

+4.2 |

|||||

Italy |

238,537 |

207,821 |

+14.8 |

|||||

Central and Eastern Europe |

592,275 |

559,946 |

+5.8 |

|||||

of which: Russia |

155,672 |

164,653 |

−5.5 |

|||||

Czech Republic |

134,926 |

126,886 |

+6.3 |

|||||

Poland |

122,622 |

104,772 |

+17.0 |

|||||

Other markets |

356,147 |

383,788 |

−7.2 |

|||||

of which: Turkey |

173,965 |

164,787 |

+5.6 |

|||||

South Africa |

78,897 |

90,659 |

−13.0 |

|||||

North America |

928,033 |

922,774 |

+0.6 |

|||||

of which: USA |

591,063 |

607,096 |

−2.6 |

|||||

Mexico |

238,946 |

211,845 |

+12.8 |

|||||

Canada |

98,024 |

103,833 |

−5.6 |

|||||

South America |

362,343 |

489,636 |

−26.0 |

|||||

of which: Brazil |

231,196 |

353,508 |

−34.6 |

|||||

Argentina |

92,257 |

97,775 |

−5.6 |

|||||

Asia-Pacific |

4,282,656 |

3,902,172 |

+9.8 |

|||||

of which: China |

3,975,071 |

3,542,467 |

+12.2 |

|||||

Japan |

83,109 |

91,153 |

−8.8 |

|||||

India |

66,046 |

69,323 |

−4.7 |

|||||

Worldwide |

9,635,484 |

9,320,687 |

+3.4 |

|||||

Volkswagen Passenger Cars |

5,980,307 |

5,823,414 |

+2.7 |

|||||

Audi |

1,867,738 |

1,803,246 |

+3.6 |

|||||

ŠKODA |

1,126,477 |

1,055,501 |

+6.7 |

|||||

SEAT |

408,703 |

400,037 |

+2.2 |

|||||

Bentley |

11,023 |

10,100 |

+9.1 |

|||||

Lamborghini |

3,457 |

3,245 |

+6.5 |

|||||

Porsche |

237,778 |

225,121 |

+5.6 |

|||||

Bugatti |

1 |

23 |

−95.7 |

|||||

COMMERCIAL VEHICLE DELIVERIES

The Volkswagen Group delivered a total of 661,513 commercial vehicles to customers worldwide in 2016, 8.5% more than in the previous year. Trucks accounted for 165,806 units (+2.4%) and buses for 17,775 units (+3.7%). Sales by the Volkswagen Commercial Vehicles brand were up 10.9% on the previous year, with 477,932 vehicles delivered. The MAN brand handed over 102,235 vehicles to customers, 0.2% fewer than in 2015, while the Scania brand’s deliveries were up 6.2% year-on-year at 81,346 units.

In Western Europe, deliveries were up 13.6% on the previous year at 418,931 vehicles as a result of the sustained economic recovery. Of this total, 327,225 were light commercial vehicles, 86,472 were trucks and 5,234 were buses. The Transporter and Caddy were the most sought-after Group models in Western European markets.

We handed over 65,436 vehicles to customers in Central and Eastern Europe in the period from January to December 2016. This was 18.2% more than in the previous year. Of this figure, 36,484 were light commercial vehicles, 28,184 were trucks and 768 were buses. In Russia, the region’s largest market, we delivered 11,300 vehicles. This was 15.4% more than in the previous year. The Transporter and the Caddy were the Group models experiencing the highest demand in Central and Eastern Europe.

In the Other markets, deliveries of Volkswagen Group commercial vehicles fell by 5.3% to a total of 70,927 units: 51,784 light commercial vehicles, 16,227 trucks and 2,916 buses.

Deliveries in North America amounted to 11,140 vehicles (+22.4%), which were handed over almost exclusively to customers in Mexico. Of this figure, 8,479 were light commercial vehicles, 669 were trucks and 1,992 were buses.

The Volkswagen Group sold a total of 59,196 units in South America (−14.2%), of which 32,258 were light commercial vehicles, 22,828 trucks and 4,110 buses. Once again, the Amarok was particularly popular. The persistently difficult economic situation and the difficult financing conditions in Brazil led to a 27.3% decrease in deliveries; 8,441 light commercial vehicles, 16,274 trucks and 1,817 buses were handed over to customers in the country.

In the Asia-Pacific region, the Volkswagen Group delivered 35,883 vehicles to customers in the reporting period; 21,702 light commercial vehicles, 11,426 trucks and 2,755 buses. This was 8.9% more than in the previous year. The Transporter and the Amarok were the most popular Group models. In China, sales were up 14.7% on the previous year at 7,071 vehicles. Of this total, 3,980 were light commercial vehicles, 2,755 were trucks and 336 were buses.

| (XLS:) |

COMMERCIAL VEHICLE DELIVERIES TO CUSTOMERS BY MARKET1 |

||||||||

|---|---|---|---|---|---|---|---|---|

|

DELIVERIES (UNITS) |

CHANGE |

||||||

|

2016 |

2015 |

(%) |

|||||

|

||||||||

|

|

|

|

|||||

Europe/Other markets |

555,294 |

498,906 |

+11.3 |

|||||

Western Europe |

418,931 |

368,622 |

+13.6 |

|||||

Central and Eastern Europe |

65,436 |

55,348 |

+18.2 |

|||||

Other markets |

70,927 |

74,936 |

−5.3 |

|||||

North America |

11,140 |

9,099 |

+22.4 |

|||||

South America |

59,196 |

68,958 |

−14.2 |

|||||

of which: Brazil |

26,532 |

36,513 |

−27.3 |

|||||

Asia-Pacific |

35,883 |

32,946 |

+8.9 |

|||||

of which: China |

7,071 |

6,165 |

+14.7 |

|||||

Worldwide |

661,513 |

609,909 |

+8.5 |

|||||

Volkswagen Commercial Vehicles |

477,932 |

430,874 |

+10.9 |

|||||

Scania |

81,346 |

76,561 |

+6.2 |

|||||

MAN |

102,235 |

102,474 |

−0.2 |

|||||

DELIVERIES IN THE POWER ENGINEERING SEGMENT

Orders in the Power Engineering segment are usually part of major investment projects. Lead times typically range from just under one year to several years, and partial deliveries as construction progresses are common. Accordingly, there is a time lag between incoming orders and sales revenue from the new construction business.

Sales revenue in the Power Engineering segment was largely driven by Engines & Marine Systems and Turbomachinery, which together generated almost three quarters of the overall revenue volume. Eight engines were delivered for a new power plant in Nicaragua, for instance. The power plant will have an output of 140 MW once it has been completed and put into operation and will cover around 10% of Nicaragua’s total energy needs.